Income built to last a lifetime

Designed to create income you can count on —

for wherever life takes you

Take out the guesswork with a Lincoln fixed indexed annuity and its built-in income benefit, Lincoln ProtectedPay® Select.1 Here's a closer look at how lifetime income works in a FIA.

Protected retirement savings and growth

- Grow future income by 10% each year2

- Capture upside potential for your account value

- Stay 100% protected from market losses

Protected lifetime income

- Count on income that will never go down

- Plan for certainty with lifetime income payments

- Add protection for a spouse

Protected legacy for loved ones

- Plan for both income and a meaningful legacy

- Leave beneficiaries the full purchase amount3

- Available for an additional cost of 0.45%

Click through each tab to see how it works in each phase of retirement.

- Protected savings and growth

- Protected lifetime income

- Protected legacy for loved ones

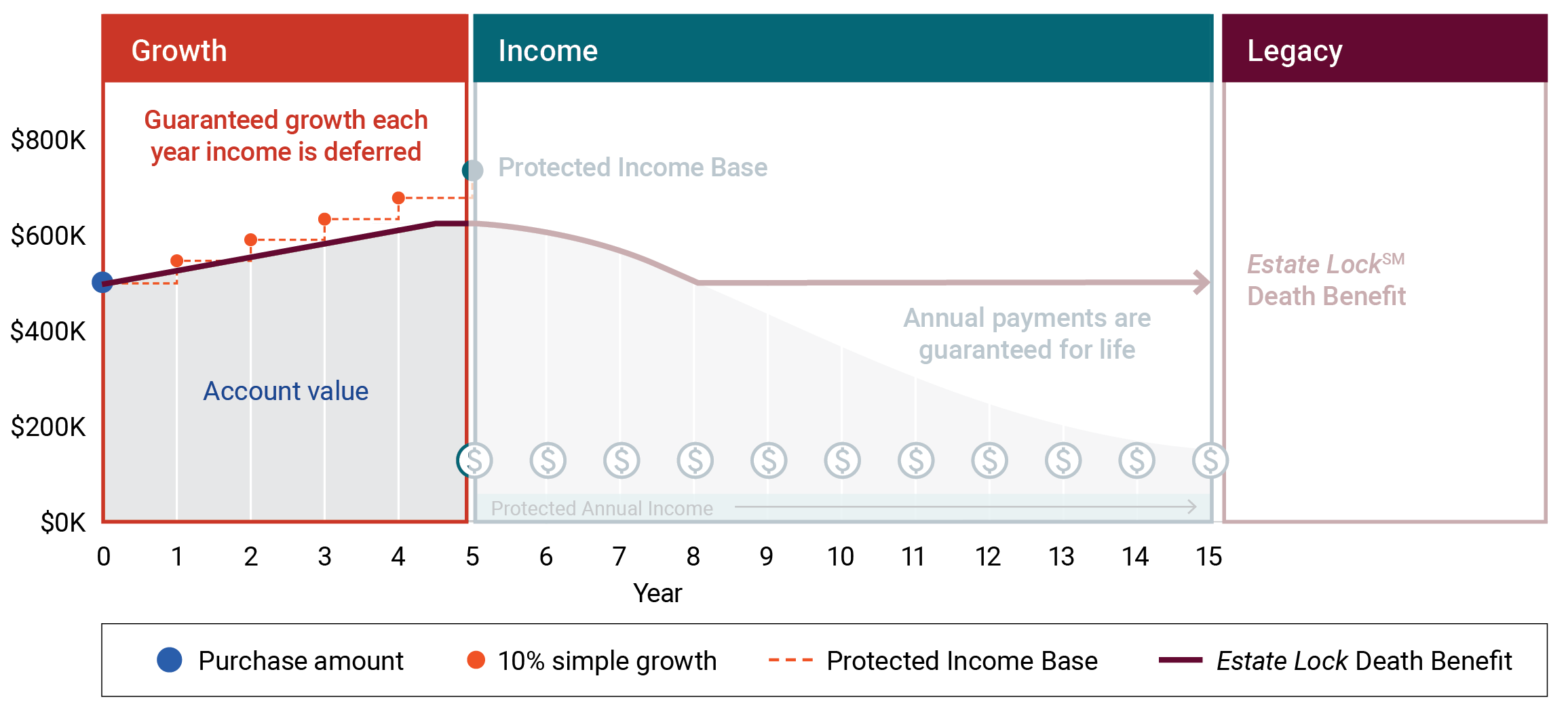

Sam, age 65, worked with his financial professional to allocate $500,000 to a fixed indexed annuity with Lincoln ProtectedPay® Select and the Estate LockSM Death Benefit. Since he’s not retiring right away, his Protected Income Base (the amount used to calculate his lifetime income) grows by 10% each year he waits to take income.

At the same time, his account value grew to over $600,000, based on the performance of the growth strategies he selected.

This chart is for illustrative purposes only. It does not reflect a specific allocation. Past performance does not guarantee future results. Guarantees are subject to the claims-paying ability of the issuer.

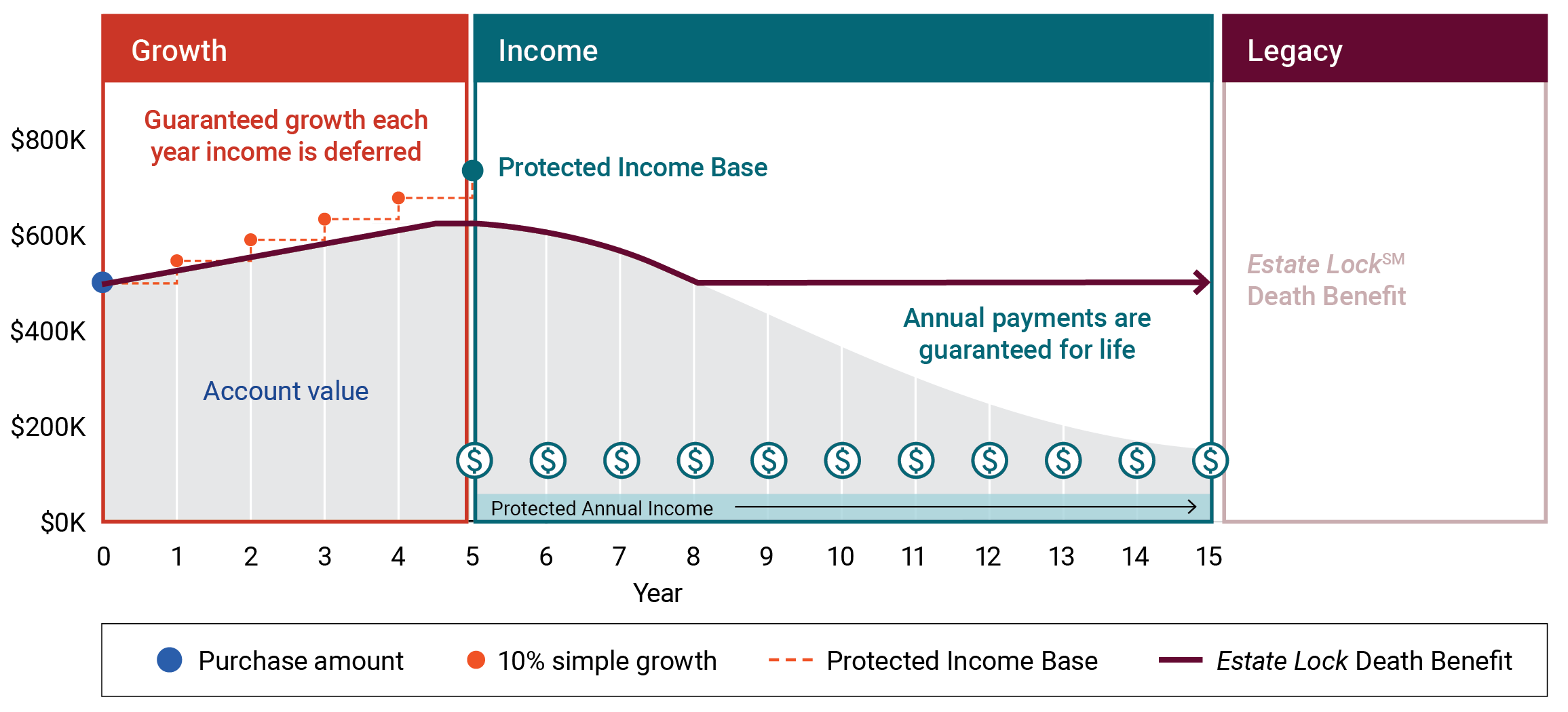

When Sam is ready to take income at age 70, his Protected Income Base has grown to $750,000. With a withdrawal rate of 6.10% based on his Protected Income Base, his Protected Annual Income payments will be $45,750 guaranteed for life.

This chart is for illustrative purposes only. It does not reflect a specific allocation. Past performance does not guarantee future results. Guarantees are subject to the claims-paying ability of the issuer.

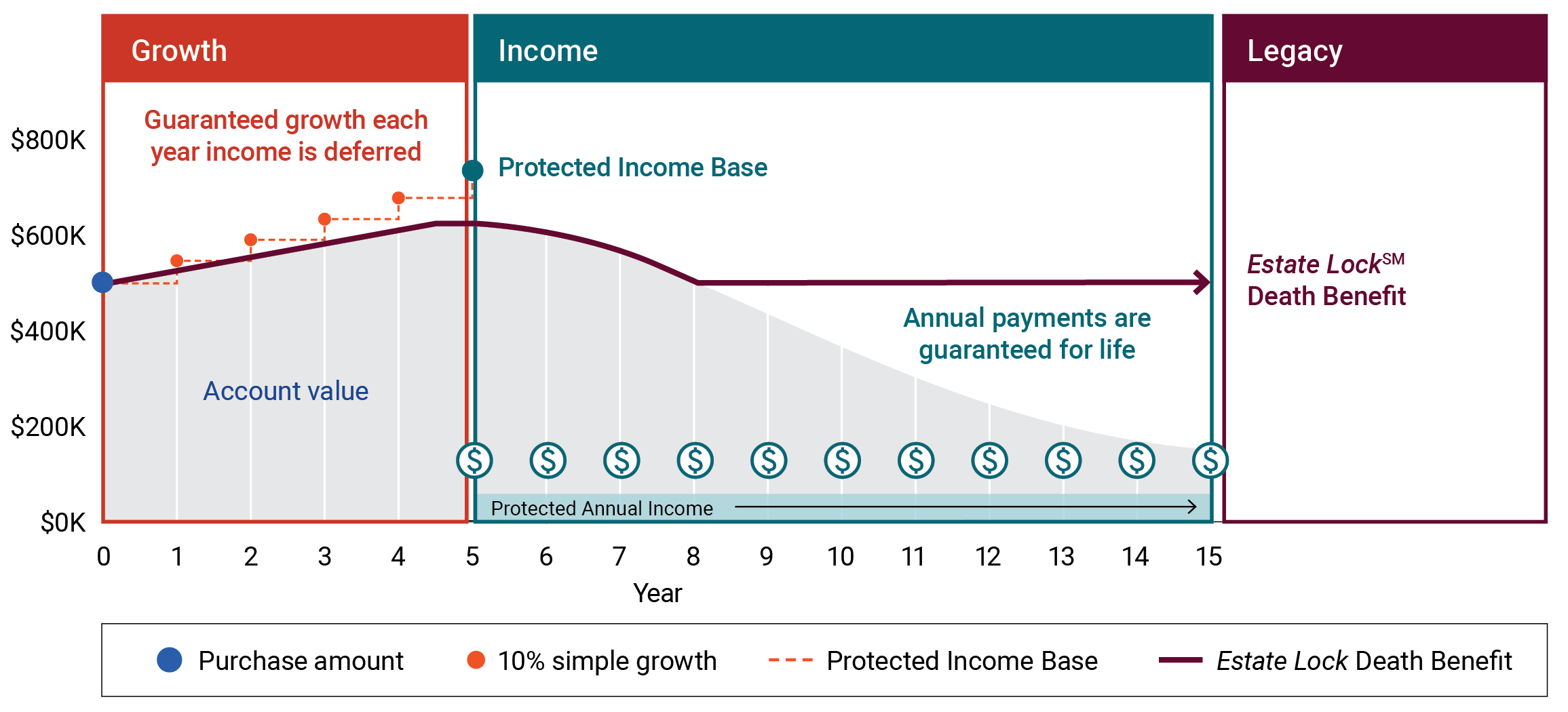

When Sam passed away ten years later, the Estate LockSM Death Benefit allowed him to leave his full purchase amount of $500,000 to his daughter since his account value was greater than zero1 — even after taking $457,500 in income — bringing the total payout in this example to $957,500. He would have passed on the account value any year it was higher than $500,000.

This chart is for illustrative purposes only. It does not reflect a specific allocation. Past performance does not guarantee future results. Guarantees are subject to the claims-paying ability of the issuer.

Explore our fixed indexed annuity income products

The products below are subject to firm and state approvals:

Lincoln ProtectedPay® Select

See income rates

Estate LockSM Death Benefit

Take a closer look1Lincoln ProtectedPay® Select is automatically included at issue for an annual cost of 1.10% single or joint (maximum annual charge is 2.25%).

2The 10% simple annual growth will continue for the earlier of 10 years or through age 85 (based on the oldest life for joint) and is not available in any year a withdrawal is taken. The Protected Income Base is not available as a separate benefit upon surrender, death or annuitization.

3In certain states, there is a cap for the Estate LockSM Death Benefit. The cap is equal to the greater of: (a) 125% of the contract’s cash surrender value, or (b) the lesser of the following two calculated amounts: i) premium(s), minus the sum of all withdrawals accumulated at an annualized interest rate of 10%; and ii) 250% of premium(s) minus the sum of all withdrawals. If your account value reaches $0, your income will continue for life but the Estate LockSM Death Benefit will terminate. Please refer to the product Disclosure Statement for a list of states where the cap applies.

Lincoln fixed indexed annuities (contract forms ICC1515-619, ICC17-622, ICC25-000702 and state variations) are issued by The Lincoln National Life Insurance Company, Fort Wayne, IN, and distributed by Lincoln Financial Distributors, Inc., a broker-dealer. The Lincoln National Life Insurance Company does not solicit business in the state of New York, nor is it authorized to do so. Contractual obligations are subject to the claims-paying ability of The Lincoln National Life Insurance Company.

Date last updated: 06/15/2026